Southeast Industrial & Warehouse Market Trends

Southeast Industrial Market Report – Q1 2026 | Cornovus Capital (Cornovuscapital)

Summary: The Southeast U.S. industrial market registered a definitive cyclical pivot in Q1 2026, with national vacancy falling from its peak, net absorption surging 52% year-over-year, and asking rents posting their first positive annual growth since 2024. The Southeast captured an outsized share of the rebound, led by Atlanta’s bulk recovery, Nashville’s sustained tightness, and port-driven absorption in Savannah and Charleston. This inflection is supported by disciplined supply, a resurgence in big-box leasing, and a reopening capital market, though it unfolds against a backdrop of reshoring demand shifts and lingering supply in specific submarkets.

Why it matters: The inflection signals a shift from a period of oversupply and rent stagnation to one of selective recovery, redefining refinancing windows, acquisition targets, and capital deployment strategies for owners and lenders across the region.

Context: This follows a multi-year supply wave and occupier hesitation, with the Southeast’s structural advantages in logistics, manufacturing reshoring, and population growth positioning it for a sharper recovery than other U.S. regions.

"Q1 2026 marked the cyclical pivot the U.S. industrial sector has been waiting for since 2022. Industry-wide tracking converged on a consistent reading: vacancy peaked, completions decelerated to multi-year lows, occupier demand held durable, and asking rents posted their first positive year-over-year prints since 2024." — CORNOVUSCAPITAL

Commentary: The report’s granularity reveals a bifurcated recovery: assets in I-85 North Atlanta or Nashville’s mid-bay segment now command pricing power, while transitional product in Charleston or South Atlanta still requires structured capital. The reshoring narrative has pragmatically shifted from pure EV to hybrid production, altering the demand profile for supplier-tier space. For capital allocators, the stable 10-year Treasury band and lean industrial CMBS distress profile create a rare window for refinancing 2020-2022 vintage debt, but sponsor quality is now the primary underwriting differentiator.

Date: May 14, 2026 12:00 AM ET

URL: https://cornovuscapital.com/southeast-industrial-market-report-q1-2026/

AI Sentiment Score: Positive (57%)

AI Credibility Score: 9.8/10 — High

Scores and text generated by AI analysis of the source article indicated.SPRING 2026 | Dallas Fort Worth Commercial Real Estate (Leedallas)

Summary: The Dallas-Fort Worth industrial real estate market shows resilience in Q1 2026, with net absorption of 9.66 million square feet and a slight vacancy rate decline to 9.21%, despite moderating from peak growth. New construction remains robust at 33.4 million square feet underway, and rents continue to rise. The market is transitioning to a more balanced, sustainable phase while maintaining its status as a premier national logistics hub.

Why it matters: DFW’s sustained industrial fundamentals signal where capital, logistics infrastructure, and corporate expansion are concentrating, offering a leading indicator for regional economic momentum and supply chain resilience in the Southeast.

Context: This follows a period of hyper-expansion in Sun Belt industrial markets, where DFW has been a primary beneficiary of supply chain reconfiguration and e-commerce growth.

"The Dallas-Fort Worth (DFW) industrial real estate market entered Q1 2026 on stable footing, continuing its shift from the rapid industrial expansion seen in recent years toward a more balanced and sustainable growth cycle." — LEEDALLAS

Commentary: The data confirms DFW’s maturation from a boom market to a steady-state engine, absorbing significant new supply while maintaining rent growth. This durability, amid declining transaction volume, suggests institutional capital views the asset class as a core holding, not a speculative play. The region’s continued construction pipeline, however, introduces a latent risk of oversupply should demand materially decelerate.

Date: April 16, 2026 12:00 AM ET

URL: https://leedallas.com/news/dallas-commercial-real-estate-industrial-market-report-spring-2026/

AI Sentiment Score: Positive (57%)

AI Credibility Score: 9.9/10 — High

Scores and text generated by AI analysis of the source article indicated.Peak Industrial Vacancy Likely in Rearview Mirror as … (Ir.Cushmanwakefield)

Summary: Cushman & Wakefield’s Q1 2026 industrial market report indicates the sector has likely passed its cyclical vacancy peak, with a national rate of 7.0% sitting 10 basis points below the Q3 2025 high. Net absorption of 40 million square feet marked the strongest first quarter since 2023, while new supply completions fell to a post-2017 low of 54 msf. The construction pipeline, however, grew for a third consecutive quarter, led by inland hubs like Memphis, St. Louis, and Charlotte. Annual asking rent growth strengthened to 2.1%, with 60% of markets reporting positive growth.

Why it matters: This signals a pivot from a supply-glut phase to a tightening market, directly impacting capital allocation, development risk, and occupier costs for logistics networks.

Context: The industrial sector has been rebalancing after a period of oversupply following the pandemic-driven expansion, with investor focus shifting to absorption rates and rent growth sustainability.

"NEW YORK–(BUSINESS WIRE)– The U.S. industrial real estate market entered 2026 on solid footing, with first-quarter fundamentals signaling a market that is stabilizing and beginning to rebalance, according to the latest market." — IR.CUSHMANWAKEFIELD

Commentary: The report’s inflection point narrative is supported by data but tempered by a rising construction pipeline; the concentration of new groundbreakings in specific inland hubs suggests capital is betting on regional divergence rather than a broad-based recovery. For occupiers, the focus on the 500,000-square-foot segment and ‘newer products’ indicates a flight to quality and operational efficiency, which could pressure older, secondary assets. The simultaneous slowdown in completions and increase in construction starts reflects developer caution meeting renewed, targeted confidence—a dynamic that could keep vacancy compression uneven across geographies.

Date: April 14, 2026 12:00 AM ET

URL: https://ir.cushmanwakefield.com/news/press-release-details/2026/Cushman--Wakefield-Market-Report-Peak-Industrial-Vacancy-Likely-in-Rearview-Mirror-as-Demand-Holds-and-Supply-Slows/default.aspx

AI Sentiment Score: Positive (50%)

AI Credibility Score: 9.9/10 — High

Scores and text generated by AI analysis of the source article indicated.Big Box Industrial Market Rebounds As Demand Strengthens (Globest)

Summary: The North American big box industrial market has shifted from a supply-driven softness to a demand-led recovery, with national vacancy falling to 10% as new leasing surged to 145.6 million square feet in the second half of 2025. This rebound is underpinned by broad demand from 3PLs, retailers, e-commerce, and reshoring activity, while a sharp 70% contraction in the construction pipeline from 2022 peaks has tightened supply. The recovery is regionally uneven, with logistics-heavy metros like Columbus and Greenville-Spartanburg leading absorption and vacancy declines, while oversupplied coastal markets like Seattle-Puget Sound continue to lag.

Why it matters: The divergence between tightening logistics hubs and lagging coastal markets signals a reallocation of capital and operational capacity within U.S. supply chains, with direct implications for infrastructure investment, labor markets, and regional economic competitiveness.

Context: This follows a period of aggressive speculative development in 2021 – 2022 that created a supply overhang, particularly in port-adjacent markets, which is now being corrected through a sharp pullback in new construction.

"The North American big box industrial market gained momentum in the second half of 2025, marking a clear shift from the softness of prior years toward a more balanced environment, according to." — GLOBEST

Commentary: The data confirms a strategic pivot in industrial real estate: capital and tenant demand are concentrating in inland logistics corridors optimized for network efficiency, not just port proximity. This geographic reweighting, visible in the stark performance gaps between Columbus and Seattle, could pressure coastal market rents and valuations until excess inventory is absorbed, while accelerating infrastructure and labor investment in the Southeast and Midwest.

Date: May 01, 2026 12:00 AM ET

URL: https://www.globest.com/amp/2026/05/01/big-box-industrial-market-rebounds-as-demand-strengthens/

AI Sentiment Score: Negative (66%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Industrial Real Estate Vacancy Stabilizes at 7.1 Percent in 2026 (Innovativelogisticsgroup.Io)

Summary: The U.S. industrial real estate market shows a clear inflection, with vacancy stabilizing at 7.1% for Q2 2026 and net absorption returning to the 50-million-square-foot range. Full-year 2025 absorption finished 16% ahead of the prior year, while new construction deliveries fell to their lowest annual total since 2017. These three converging signals—stabilized vacancy, rising absorption, and constrained new supply—indicate a tightening freight environment is forming for the back half of 2026 and into 2027.

Why it matters: For logistics operators and investors, this is a leading indicator of freight demand and pricing power, offering a tactical planning window before the broader market reacts.

Context: Industrial vacancy and freight demand are closely coupled, with a lag. After two years of rising vacancy and soft absorption, this quarter marks a reversal of that trend.

"Industrial vacancy at 7.1 percent is not historically tight, but it is no longer climbing, and that is the meaningful inflection." — INNOVATIVELOGISTICSGROUP.IO

Commentary: The bifurcation in vacancy rates—with small-box space under 50,000 sq ft at ~4.8% and big-box over 300,000 sq ft near 10%—creates a segmented opportunity. Small carriers can exploit tighter submarkets and lanes while larger operators remain burdened by excess big-box capacity. The deliberate supply constraint, with deliveries down 35% from 2024, shifts leverage from developers and shippers back to asset-holding operators, setting the stage for rate firming and strategic lane consolidation in H2 2026.

Date: April 30, 2026 12:00 AM ET

URL: https://innovativelogisticsgroup.io/small-fleet-growth/industrial-real-estate-vacancy-stabilizes-at-7-1-percent-in-2026-how-small-carriers-should-read-the-warehouse-market-signal-for-lane-strategy/

AI Sentiment Score: Negative (80%)

AI Credibility Score: 8.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Industrial Market Updates & Insights (Cornovuscapital)

Summary: Q1 2026 data confirms a national industrial real estate recovery, with the Southeast U.S. leading the rebound. The region captured disproportionate absorption and investment, driven by port infrastructure, logistics networks, and a concentration of reshoring megaprojects. Key markets like Atlanta, Charlotte, Nashville, Savannah, and Charleston showed strong vacancy declines and rent growth.

Why it matters: The Southeast’s industrial dominance signals a structural shift in U.S. manufacturing and logistics geography, with implications for capital allocation, corporate site selection, and regional economic power.

Context: This follows a multi-year capital cycle focused on reshoring and supply chain resilience, with the Southeast securing a critical mass of anchor investments that now drive secondary demand.

"Q1 2026 marked the cyclical pivot the U.S. industrial sector has been waiting for since 2022. National vacancy moved off its cyclical peak to approximately 7.0%, net absorption registered approximately 40 million." — CORNOVUSCAPITAL

Commentary: The data validates the Southeast as the primary beneficiary of the reshoring narrative, moving from speculative pipeline to operational reality. This concentration creates a self-reinforcing ecosystem that will likely drain talent and capital from legacy industrial regions. The risk is regional overheating and infrastructure strain, but the near-term momentum appears locked in by committed capital from automotive and battery manufacturing anchors.

Date: May 14, 2026 12:00 AM ET

URL: https://cornovuscapital.com/industrial-market-update/

AI Sentiment Score: Negative (75%)

AI Credibility Score: 7.0/10 — Medium

Scores and text generated by AI analysis of the source article indicated.Q4 2025 Global Logistics Real Estate Outlook | Prologis Research (Youtube)

Summary: Prologis Research reports a cyclical inflection in global logistics real estate for Q4 2025, marked by strengthening demand, disciplined supply, and rent stabilization. Key indicators include a 12% quarterly increase in global net absorption, with U.S. absorption exceeding completions for the first time since 2022. Vacancy rates have likely peaked, and global values rose 0.6% quarter-over-quarter, driven by gains in the U.S. and Latin America.

Why it matters: The data signals a durable recovery in a critical infrastructure sector, with implications for capital allocation, industrial land values, and supply chain investment decisions across the Southeast and other high-growth regions.

Context: This follows a prolonged period of oversupply and softening rents post-pandemic, where development starts outpaced absorption. The inflection suggests a return to landlord-favorable conditions in key markets.

"Alejandra Chavellas of Prologis Research shares a global logistics real estate market update, covering the cyclical inflection underway as vacancy peaks, demand strengthens and market fundamentals turn more constructive. In this Logistics." — YOUTUBE

Commentary: The shift from oversupply to absorption-led recovery will concentrate development opportunities in primary logistics corridors, particularly in the Southeast where port expansion and manufacturing reshoring intersect. Capital chasing stabilized yields will likely accelerate asset price appreciation in markets like Atlanta and Savannah before new supply can respond, creating a window for strategic land banking.

Date: May 18, 2026 12:00 AM ET

URL: https://www.youtube.com/watch?v=1OxjLAPtdF8

AI Sentiment Score: Positive (71%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.How Tariffs Are Reshaping Warehouse Demand in 2026 | WareCRE (Warecre)

Summary: Tariffs are accelerating industrial real estate demand through two distinct mechanisms: short-term inventory front-loading ahead of rate hikes and long-term manufacturing reshoring. National industrial absorption is projected to surge from 155 million SF in 2025 to 200 million SF in 2026. The Southeast and Central U.S. are primary beneficiaries of reshoring investment, while a severe shortage of small-bay warehouse space (under 10,000 SF) is creating acute pressure for the businesses most exposed to tariff costs.

Why it matters: For regional economic observers, this signals a tangible, near-term redirection of capital and logistics infrastructure into the Southeast, with specific asset classes becoming critical bottlenecks.

Context: This follows a multi-year trend of supply chain reconfiguration, but the tariff catalyst is now quantifiable in absorption forecasts and vacancy rate divergences between small-bay and big-box space.

"- Tariffs are driving warehouse demand through two channels: short-term inventory front-loading (businesses pre-buying goods before rates increase) and long-term reshoring of manufacturing. – National industrial absorption is forecast to hit 200M." — WARECRE

Commentary: The bifurcation in vacancy rates—3-4% for small-bay versus 7-8% for big-box—reveals the operational scale of affected firms: smaller importers and manufacturers are driving the immediate crunch. This creates a pricing and development arbitrage opportunity in secondary logistics markets, while potentially straining local industrial zoning and last-mile logistics networks. The explicit call for businesses to ‘calculate your tariff-adjusted inventory needs’ underscores a shift from speculative leasing to defensive operational calculus.

Date: April 28, 2026 12:00 AM ET

URL: https://warecre.com/cre-insights/industrial-101/tariffs-reshaping-warehouse-demand-2026/

AI Sentiment Score: Neutral (50%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Miami Warehouse Market Report 2026 | Vacancy, Rents & Outlook (Warecre)

Summary: Miami’s industrial vacancy rate has risen to 7.0-7.2% in Q1 2026, its highest point in five years, driven by a historic construction pipeline delivering new supply. Leasing activity remains steady, indicating the rise is supply-driven rather than a demand collapse. Rents have softened slightly overall, but Class A distribution and small-bay warehouse segments show resilience. The construction pipeline is now declining, signaling a peak in new supply and a forecast for vacancy to plateau and begin tightening by late 2026.

Why it matters: This recalibration signals a shift from a hyper-constrained market to a more balanced one, affecting capital allocation for industrial developers and rental strategies for logistics tenants in a key Southeast gateway.

Context: South Florida’s warehouse market had experienced years of sub-5% vacancy and double-digit rent growth, fueled by pandemic-era logistics demand and e-commerce expansion.

"Key Takeaways – Miami industrial vacancy reached 7.0-7.2% in Q1 2026 — the highest in five years — but the rise is supply-driven, not a demand collapse. Leasing activity held steady. -." — WARECRE

Commentary: The bifurcation between big-box and small-bay performance underscores a structural undersupply in flexible, last-mile logistics space that developers are not addressing at scale. This will concentrate investor interest and tenant competition in the sub-10,000 SF segment, while large distribution landlords face a period of flat rents and selective concessions. The declining pipeline suggests a self-correcting mechanism, but the timing of the tightening hinges on absorption rates normalizing to pre-2023 levels.

Date: April 28, 2026 12:00 AM ET

URL: https://warecre.com/cre-insights/market-property-insights/miami-warehouse-market-report/

AI Sentiment Score: Neutral (33%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.The Outlier in a Softening Industrial Market – Site Selection Group (Info.Siteselectiongroup)

Summary: The U.S. industrial real estate market is softening, with national vacancy rising to 7.6% and overall availability near 9.6%. However, shallow bay industrial properties (under 50,000 sq ft) are an outlier, maintaining a vacancy rate below 5% with faster leasing times. This divergence is driven by sustained tenant demand, a limited new supply pipeline, and the stability of multitenant buildings, creating intense competition for smaller tenants.

Why it matters: For regional economic observers and investors, this signals where capital and operational pressure are concentrating, highlighting a durable, undersupplied asset class amid broader market weakness.

Context: This follows a post-pandemic correction from historically low vacancies, revealing a structural bifurcation within the industrial sector based on building scale and tenant profile.

"As discussed in one of Site Selection Group’s recent blogs, the United States has now experienced three consecutive years of rising vacancy across the industrial real estate market. The national vacancy rate." — INFO.SITESELECTIONGROUP

Commentary: The resilience of shallow bay properties underscores a shift toward servicing localized, last-mile, and small-to-midsize business logistics, which are less sensitive to macroeconomic swings in big-box distribution. This could pressure regional development incentives toward infill and redevelopment, while institutional capital may further segment its industrial allocations. Smaller tenants, particularly in the Southeast’s growing secondary markets, will face higher occupancy costs and reduced optionality, potentially affecting local business expansion plans.

Date: April 13, 2026 12:00 AM ET

URL: https://info.siteselectiongroup.com/blog/the-outlier-in-a-softening-industrial-market

AI Sentiment Score: Negative (66%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Snapshot of Industrial Market for Q1 | MHL News (Mhlnews)

Summary: The U.S. industrial real estate market is stabilizing in Q1 2026, with demand positive in nearly 70% of markets and vacancy holding at 7.4%. New supply and absorption are rebalancing, with the South accounting for 65% of national demand. Construction activity appears to have bottomed out, while rent growth has plateaued, showing resilience in inland markets like Houston and Dallas-Fort Worth despite declines in some coastal regions.

Why it matters: The rebalancing signals a shift from speculative expansion to demand-driven development, with capital and logistics operations concentrating in the Southeast, particularly Texas and Georgia.

Context: This follows a period of rapid industrial expansion and supply chain reconfiguration post-pandemic, where vacancy rates rose sharply in 2023-2024.

"The South accounted for 65% of this demand (28M SF), with markets such as Atlanta, Dallas-Fort Worth, Houston, and Charleston each exceeding 3M SF of net absorption for the quarter." — MHLNEWS

Commentary: The data confirms the Southeast’s structural advantage in logistics, drawing capital and tenant commitments away from higher-cost coastal hubs. The plateau in national rents, juxtaposed with double-digit growth in Houston, indicates a durable repricing of industrial space based on operational cost and proximity to growing consumer bases, not just port adjacency. This rebalancing could pressure developers in oversupplied markets to pivot to build-to-suit, while institutional capital likely reallocates to Sun Belt portfolios.

Date: April 20, 2026 12:00 AM ET

URL: https://www.mhlnews.com/warehousing/news/55371684/snapshot-of-industrial-market-for-q1

AI Sentiment Score: Negative (55%)

AI Credibility Score: 9.8/10 — High

Scores and text generated by AI analysis of the source article indicated.Industrial REITs: Tenant Demand & Leasing Benefit … (Reit)

Summary: Industrial REIT fundamentals are being driven by structural e-commerce demand, which requires roughly triple the warehouse space of brick-and-mortar retail, according to Green Street. Despite a 15-quarter run where supply has outpaced demand, net absorption is rising from its Q4 2023 low, with vacancy rates near a peak. Prologis reports the Iran conflict has not significantly disrupted demand, contrasting with the immediate leasing pause after the 2025 tariff announcements. Large-scale logistics, particularly warehouses over 500,000 sq ft for last-mile distribution, are performing strongly, with Amazon alone absorbing nearly 20% of U.S. net absorption in 2025.

Why it matters: For investors and operators in Southeast industrial real estate, the data signals a turning point in the supply-demand balance, with geopolitical and trade policy shocks now being absorbed by the structural tailwind of e-commerce logistics.

Context: Industrial vacancy has been trending upward since mid-2022, but the underlying demand driver—the space-intensive nature of e-commerce fulfillment—appears robust enough to begin tightening the market.

"Green Street also estimates that online sales require around three times more warehouse space than brick‑and‑mortar retail." — REIT

Commentary: The core investment thesis for industrial REITs is no longer just about cyclical growth but the permanent capital intensity of modern retail. The sector’s resilience to the Iran conflict, compared to its sensitivity to tariffs, indicates demand is now anchored in domestic logistics architecture rather than global trade flows. This suggests capital allocation will continue to favor large, last-mile facilities in population-dense corridors, with the Southeast likely seeing concentrated investment as reshoring and e-commerce converge.

Date: May 06, 2026 12:00 AM ET

URL: https://www.reit.com/news/articles/industrial-reits-tenant-demand--leasing-benefit-fundamentals

AI Sentiment Score: Positive (50%)

AI Credibility Score: 7.0/10 — Medium

Scores and text generated by AI analysis of the source article indicated.Mizuho’s Vikram Malhotra Sees Logistics Real Estate in Early … (Reit)

Summary: Mizuho Securities analyst Vikram Malhotra argues the logistics real estate sector is in the early stages of a new upcycle, with big-box demand from firms like Walmart and Amazon driving performance. He sees sector vacancy peaking near 7.5% before a modest decline, but notes real rent growth requires vacancy to fall to about 6%, a milestone at least a year away. Global instability is strengthening reshoring trends and supporting robust annual demand projections of 150-200 million square feet, though decision timelines have lengthened.

Why it matters: For investors and operators in Southeast industrial real estate, this signals the timing of rent growth inflection and the resilience of underlying demand despite macroeconomic volatility.

Context: The logistics sector has been a primary beneficiary of e-commerce expansion and supply chain reconfiguration, with vacancy and rent trends serving as key indicators of cycle positioning.

"Until we see vacancy trend to about 6%, I think it’ll be really hard to see real rent growth…I think we’re at least a year away from a very strong market trend." — REIT

Commentary: Malhotra’s analysis provides a calibrated timeline, separating near-term spot demand strength from the delayed pricing power needed for a ‘very strong’ market. The emphasis on reshoring as a structural tailwind, even amid instability, suggests the Southeast’s industrial base is a direct beneficiary of supply chain re-architecting, not just cyclical inventory swings. The extended lease closing times paired with high proposal volumes indicate a market where capital is cautious but committed, setting the stage for a measured, demand-led recovery rather than a speculative boom.

Date: May 07, 2026 12:00 AM ET

URL: https://www.reit.com/news/podcasts/mizuhos-vikram-malhotra-sees-logistics-real-estate-early-stages-new-upcycle

AI Sentiment Score: Positive (62%)

AI Credibility Score: 7.0/10 — Medium

Scores and text generated by AI analysis of the source article indicated.This large warehouse campus south of Atlanta won’t sit … (Ajc)

Summary: The Atlanta industrial real estate market, a post-pandemic construction leader, is recalibrating after a period of oversupply. Vacancy rates, which peaked above 10% in mid-2025 after a building frenzy, have begun to decline, settling at 9.6% in March. Rent growth has slowed significantly from the 20%+ annual increases seen earlier, now at 2.3% year-over-year. The market is showing resilience with recent large leases, such as Sabert’s, indicating absorption capacity and a return to measured new construction.

Why it matters: This signals a maturation of the Southeast’s industrial boom, revealing its cyclical nature and capacity to absorb shocks, which informs capital allocation and risk assessment for logistics, real estate, and manufacturing sectors.

Context: The Southeast, particularly Atlanta, became a primary beneficiary of supply chain reconfiguration and e-commerce growth post-2020, leading to an unprecedented industrial construction wave that risked overshooting demand.

"Those projects had a queue of companies champing at the bit to occupy those warehouses as soon as possible. But the frenzy led to an oversupply of new space, leaving some new." — AJC

Commentary: The market is demonstrating a classic supply-demand correction, not a structural collapse. The return to construction at lower vacancy rates suggests developers see a sustainable floor, but the sharp deceleration in rent growth indicates pricing power has normalized. This cyclical stability, amid global headwinds, reinforces Atlanta’s position as a resilient logistics hub, though future growth will be more disciplined and margin-sensitive than the previous boom.

Date: May 06, 2026 12:00 AM ET

URL: https://www.ajc.com/business/2026/05/this-large-warehouse-campus-south-of-atlanta-wont-sit-empty-much-longer/

AI Sentiment Score: Positive (45%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Charlotte gains $200M logistics hub and more than 200 jobs (Charlotteobserver)

Summary: Averitt Express will build a $200 million regional campus on 104 acres near Charlotte Douglas International Airport, consolidating all five of its services, including distribution and fulfillment. The project will add 211 positions over four years with an average salary of $81,769, with construction slated for completion by 2028. This investment reinforces Charlotte’s strategic push to become a major logistics hub anchored by its airport infrastructure.

Why it matters: This capital commitment signals sustained corporate confidence in Charlotte’s logistics cluster, directly affecting regional job composition, commercial real estate demand near transport nodes, and competitive positioning against other Southeastern hubs.

Context: Charlotte ranked second nationally for total job growth in 2025, and the region has recently secured pledges for over 2,500 new positions across financial services, tech manufacturing, and aviation, building on an existing logistics workforce of approximately 89,000.

"A national transportation and supply chain management company is building a $200 million campus near the Charlotte airport and adding over 200 jobs to the market. Averitt Express will transform a 104-acre." — CHARLOTTEOBSERVER

Commentary: The scale and integrated-service nature of the campus indicates a shift from pure transport to higher-value logistics orchestration within the region. This could pressure talent markets for mid-skill operational roles and likely attract ancillary service firms, further densifying the airport-centric ecosystem. The timing—amid broader national job growth—suggests Charlotte’s diversification strategy is gaining momentum, though it also increases exposure to cyclical freight demand.

Date: April 29, 2026 12:00 AM ET

URL: https://www.charlotteobserver.com/news/business/article315571676.html

AI Sentiment Score: Positive (57%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Industrial Development in 2026: 3 Things Driving Location Decisions (Locationgeorgia)

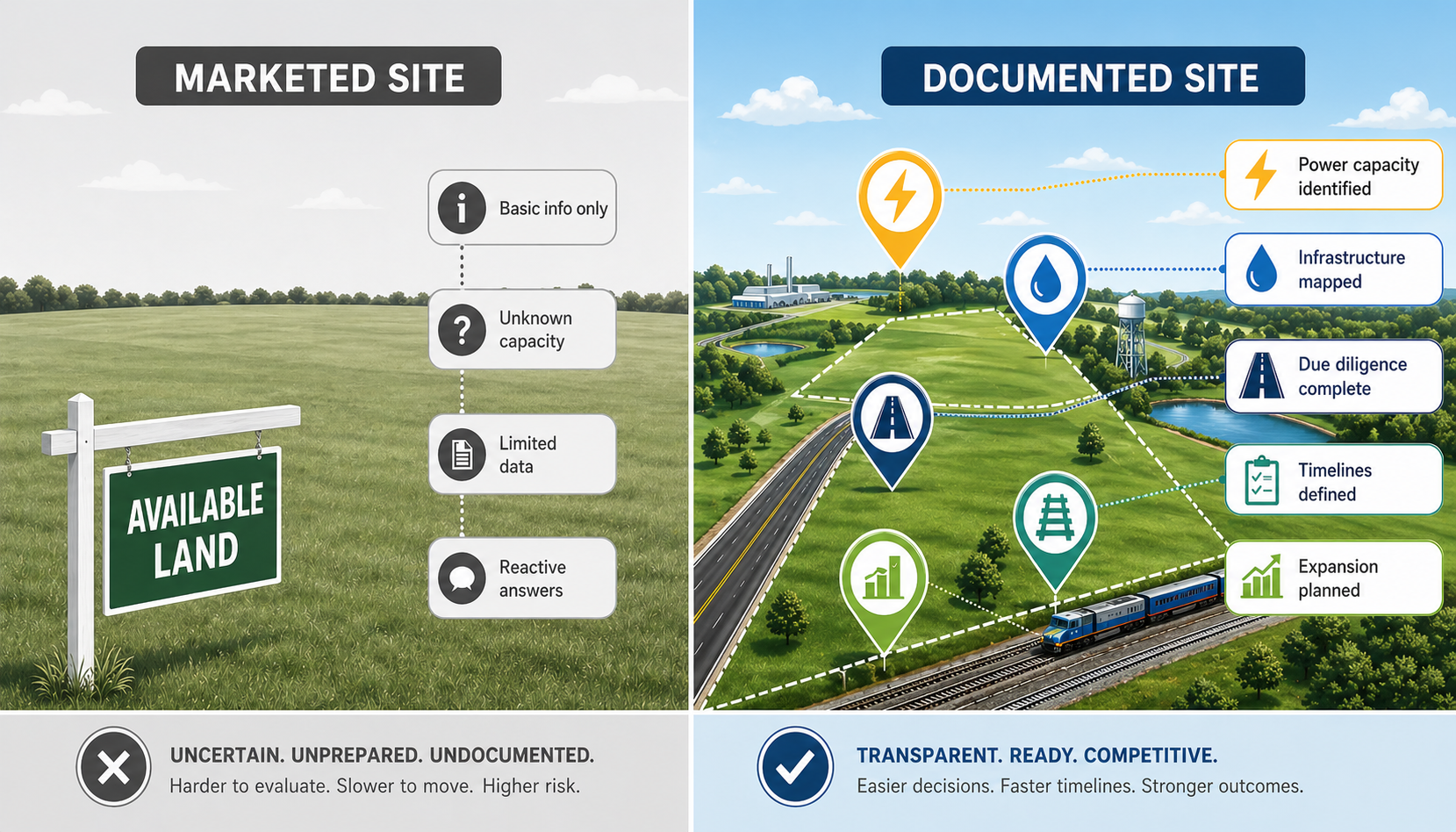

Summary: A 2026 advisory for economic developers in the Southeast frames industrial site selection around three core drivers: Power, Predictability, and Optionality. It argues that power availability has shifted from a late-stage utility check to a primary gatekeeper, requiring communities to audit site capacity, timelines, and scalability upfront. The guidance emphasizes creating transparent ‘evidence packets’ and aligning utility partners early to reduce execution risk for prospects in advanced manufacturing, logistics, and data infrastructure.

Why it matters: This signals a structural shift in capital allocation, where industrial investment will concentrate in regions that can credibly suggest and scale energy delivery, potentially accelerating divergence between prepared and unprepared markets.

Context: This reflects the operationalization of broader trends: the energy intensity of AI/data centers, reshoring’s infrastructure demands, and investor aversion to execution risk post-supply chain shocks.

"Across industries, companies in advanced manufacturing, logistics, and data infrastructure aren’t necessarily looking for the perfect location anymore. They’re looking for locations that reduce risk, preserve flexibility, and give them confidence in." — LOCATIONGEORGIA

Commentary: The memo formalizes a market reality: the utility is now a strategic partner, not a vendor. Communities that fail to produce auditable, utility-backed power snapshots will be screened out before negotiations begin. This creates a first-mover advantage for regions like Georgia’s industrial corridors, where coordinated planning with Southern Company or Oglethorpe Power can be packaged as a product. The secondary effect is a potential crowding-out of smaller, less capital-intensive projects from these priority sites as capacity is reserved for large, scalable loads.

Date: April 29, 2026 12:00 AM ET

URL: https://www.locationgeorgia.com/industrial-location-decisions-april-2026/

AI Sentiment Score: Negative (66%)

AI Credibility Score: 7.0/10 — Medium

Scores and text generated by AI analysis of the source article indicated.How infrastructure and cost are influencing Raleigh-Durham … (Capitalanalyticsassociates)

Summary: The Raleigh-Durham metro area continues to exhibit robust growth, ranking among the nation’s fastest-growing regions with significant capital investment. However, this expansion is now confronting acute physical constraints: a projected 60% rise in statewide electricity demand by 2040 is straining power grids, while the construction sector faces a national labor shortfall of hundreds of thousands of workers. These pressures are already redirecting development activity to peripheral counties like Johnston and Greenville, where land is available but infrastructure readiness lags.

Why it matters: The Southeast’s premier tech and research hub is hitting capacity limits that could force capital reallocation, reshape regional development patterns, and test the viability of continued reshoring investments.

Context: This reflects a broader national pattern where post-pandemic migration and industrial policy-driven investment are overwhelming legacy infrastructure in high-growth regions, creating a secondary tier of emerging development corridors.

"Electricity demand across North Carolina could rise by as much as 60% by 2040, placing added pressure on already constrained networks and pushing developers and end users toward outer markets such as Johnston County and Greenville, where larger sites are available but often require additional investment to become viable." — CAPITALANALYTICSASSOCIATES

Commentary: The Triangle’s success is now its primary bottleneck. The shift to outer markets is not organic decentralization but a forced retreat, indicating that infrastructure, not talent or policy, is becoming the decisive factor for site selection. This will test the resilience of the region’s growth model and could accelerate capital flight to more prepared Southeastern metros if upgrades lag.

Date: April 15, 2026 12:00 AM ET

URL: https://capitalanalyticsassociates.com/how-infrastructure-and-cost-are-influencing-raleigh-durham-development/

AI Sentiment Score: Negative (50%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Data centers vs. warehouses is Southeast Georgia’s new … (Statesboroherald)

Summary: Communities in Southeast Georgia’s Bryan, Bulloch, Effingham, and Liberty counties, having previously contended with warehouse development debates, are now anticipating a potential pivot toward data center projects. While no formal proposals are currently on the table, a state audit analysis indicates the average data center project in Georgia is valued at approximately $2.3 billion, generating nearly $28 million in annual property tax revenue. Proponents highlight the high-value tax base and reduced truck traffic compared to logistics hubs, while critics warn of intensified strain on local water and power resources, alongside the deferred fiscal benefits due to common tax abatement structures.

Why it matters: This signals a shift in the region’s industrial development calculus, where local governments must weigh immediate infrastructure and environmental costs against long-term, high-value tax revenue, with implications for land use, utility planning, and fiscal policy.

Context: This follows a broader national trend of data center expansion straining regional grids and water resources, while states and localities compete with aggressive incentive packages to attract capital-intensive tech infrastructure.

"An analysis for the Georgia Department of Audits and Accounts, released in December 2025, reported the average value for each data center project across the state approached $2.3 billion, leading to an average of nearly $28 million in annual property tax proceeds per project." — STATESBOROHERALD

Commentary: The core tension is between a deferred-revenue model and immediate resource depletion. Counties must now model net present value of abated tax streams against hard infrastructure upgrades for power and water, a calculation far more complex than for traditional warehousing. The absence of current proposals is a strategic pause, allowing local planners to design utility agreements and incentive cliffs that protect municipal balance sheets before the first site plan is filed.

Date: May 21, 2026 12:00 AM ET

URL: https://www.statesboroherald.com/local/data-centers-vs-warehouses-is-southeast-georgias-new-growth-debate/

AI Sentiment Score: Neutral (33%)

AI Credibility Score: 10.0/10 — High

Scores and text generated by AI analysis of the source article indicated.Distribution Center Underwriting & Last-Mile Logistics (Apers.App)

Summary: The 2022-2023 industrial construction wave is being absorbed, with national vacancy stabilizing in the 7-8% range and rent growth turning positive after a prolonged flat period. The recovery is being driven by big-box leasing from 3PLs and Amazon, while fundamentals diverge sharply based on port dynamics, favoring East Coast hubs like Savannah and Charleston over pressured West Coast markets. Senior debt markets continue to price industrial as the strongest commercial real estate collateral.

Why it matters: The absorption of the supply wave and return of rent growth signals a turning point in the industrial cycle, with capital allocation and development now pivoting toward regions with structural trade advantages.

Context: This follows a period of record construction completions and a subsequent vacancy peak, against a backdrop of shifting global trade routes, Panama Canal constraints, and post-2024 port share rebalancing between coasts.

"The cross-cut of CBRE, JLL, Cushman, Prologis, NAIOP, Newmark, and Trepp converges on the same read: the 2022–2023 supply wave is being absorbed, big-box leasing is driving the recovery, rent growth has returned, and the senior debt market continues to price industrial as the strongest collateral in CRE." — APERS.APP

Commentary: The data confirms a regional bifurcation: capital and tenants are consolidating in Southeast infill and East Coast port markets, structurally weakening the Inland Empire’s dominance. For institutional portfolios like EastGroup Properties, this validates a Sunbelt-infill strategy, but the high vacancy in the distribution & logistics sub-segment (12.7% per Cushman) indicates ongoing pressure in pure last-mile assets, suggesting the recovery is not uniform across industrial subtypes.

Date: May 22, 2026 12:00 AM ET

URL: https://apers.app/learn/asset-classes/industrial/logistics-distribution-ecommerce-sensitivity

AI Sentiment Score: Positive (71%)

AI Credibility Score: 7.0/10 — Medium

Scores and text generated by AI analysis of the source article indicated.Post ID: cdb1ded7